U.S. futures rose with shares Tuesday as optimism that financial reopenings will enhance progress outweighed concern a couple of pickup in virus instances in components of Asia. The greenback dipped and oil gained.

Contracts on all three U.S. fairness benchmarks superior, led by these on the Nasdaq 100 Index, signaling a rebound in tech shares. Retailers Walmart Inc. and Macy’s Inc. climbed in premarket buying and selling after elevating their full-year steerage, whereas Residence Depot Inc. gained as its outcomes beat estimates. Commodity and journey shares boosted the Stoxx Europe 600 Index, whereas Asian equities additionally climbed.

The greenback fell towards a four-month low, whereas U.S. 10-year Treasuries rose. Brent crude at one level topped $70 a barrel in London for the primary time since March on indicators that reopenings are boosting demand.

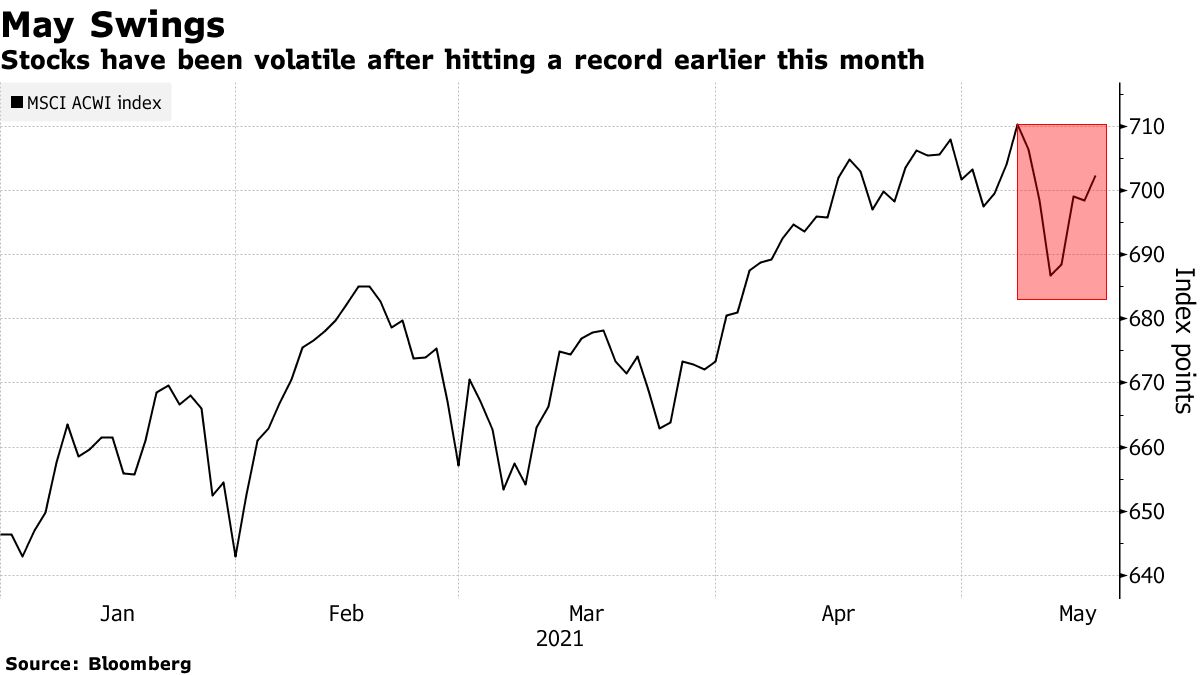

Shares have been risky after climbing to a document in early Could as buyers assessed financial progress prospects towards a Covid-19 resurgence in international locations together with India. Minutes from the newest Federal Reserve assembly, due Wednesday, might supply buyers clues on inflation stress and hints of a timeline for tapering stimulus.

Fed Vice Chair Richard Clarida stated Monday that the weak U.S. jobs report confirmed the economic system had not but reached the edge to warrant scaling again asset purchases.

International investor sentiment is “unambiguously bullish,” Financial institution of America Corp. strategists led by Michael Hartnett stated, citing the agency’s newest fund supervisor survey. Inflation topped the listing of the largest tail dangers, adopted by a bond market taper tantrum and asset bubbles, whereas Covid-19 was solely in fourth place.

Elsewhere, Bitcoin was regular following volatility spurred by feedback from Tesla Inc.’s Elon Musk. Coinbase International Inc. fell in premarket buying and selling after Monday’s drop beneath the reference worth utilized in its April direct itemizing. AMC Leisure Holdings Inc. superior 7%, extending its longest rally since 2019.

Listed below are some key occasions this week:

- The Fed publishes minutes from its April assembly Wednesday, which can present clues to officers’ views on the restoration and the way they outline “transitory” in terms of inflation

- EIA crude oil stock report Wednesday

- St. Louis Fed President James Bullard and Atlanta Fed President Raphael Bostic to talk at separate occasions Wednesday

- IMF Managing Director Kristalina Georgieva and ECB President Christine Lagarde communicate on the Vienna Financial Dialogue Thursday

- Australia unemployment fee Thursday

- Euro-area finance ministers and central financial institution chiefs maintain a casual assembly. A bigger group of EU finance ministers and central financial institution chiefs will meet Could 22

These are a number of the major strikes in markets:

Shares

- Futures on the S&P 500 rose 0.2% as of 8:31 a.m. New York time

- Futures on the Nasdaq 100 rose 0.5%

- Futures on the Dow Jones Industrial Common rose 0.2%

- The Stoxx Europe 600 rose 0.3%

- The MSCI World index rose 0.5%

Currencies

- The Bloomberg Greenback Spot Index fell 0.4%

- The euro rose 0.6% to $1.2221

- The British pound rose 0.5% to $1.4203

- The Japanese yen rose 0.3% to 108.92 per greenback

Bonds

- The yield on 10-year Treasuries declined one foundation level to 1.64%

- Germany’s 10-year yield declined one foundation level to -0.13%

- Britain’s 10-year yield declined one foundation level to 0.85%

Commodities

- West Texas Intermediate crude rose 0.5% to $67 a barrel

- Gold futures rose 0.2% to $1,872 an oz.

— With help by Andreea Papuc